The $147 Billion Robotaxi Question: Who Wins the Fleet Economics Race?

This article analyzes the economics of robotaxis and explains why autonomous ride-hailing is not just a technology breakthrough but a business model reset. It examines robotaxi ride-volume growth, fleet utilization, city density, operating costs, charging economics, remote monitoring, and the shift from ride-hailing marketplaces to autonomous fleet orchestration.

The $147 Billion Robotaxi Question: Who Wins the Fleet Economics Race?

May 12, 2026 • 11 min read

Highlights

Global Robotaxi market is projected to grown from $ 0.61 Bn in 2025 to $ 147 Bn by 2033, implying a 99.1% CAGR[i]

Robotaxis are not a better ride-hailing app — they are a capital-intensive fleet economics business.

Robotaxi viability depends on whether operators can overcome high capital costs, remote monitoring, maintenance, insurance, sensor servicing, data processing, and low utilization risk.

Future advantage will likely come from dense service-area design, high vehicle uptime, low empty mileage, charging efficiency, and backend fleet intelligence — not just autonomy software.

Ride-hailing scaled first as an asset-light marketplace: aggregate demand, improve matching, and rely on drivers or fleet partners to absorb much of the asset risk.

Robotaxis change the operating logic. The competitive question shifts from “Who can match riders and drivers most efficiently?” to “Who can finance, deploy, operate, and utilize autonomous fleets most productively?”

But the economics are not yet solved. Recent research notes that robotaxi operations still appear dependent on investor subsidies because fully burdened costs remain high, including vehicle capital costs, R&D, remote monitoring, sensor servicing, maintenance, insurance, and data processing.[ii] The next mobility winners may not simply be the companies with the best app. They may be the companies that can make autonomous fleet economics work at city scale.

1. The first ride-hailing playbook was asset-light

For more than a decade, ride-hailing platforms scaled primarily as marketplace businesses.

The logic was powerful because it was relatively simple: aggregate rider demand, attract driver supply, improve matching efficiency, increase utilization, and expand city-level network density. The platform controlled the demand interface and the matching engine, while much of the supply-side asset burden sat outside the platform.

Drivers, fleet owners, leasing firms, and financing partners absorbed a large share of vehicle ownership risk, financing burden, maintenance responsibility, insurance exposure, and depreciation. Ride-hailing companies could therefore operate as orchestration layers on top of fragmented supply networks.

That model shaped the economics of the category. The most important questions were marketplace questions: How quickly can riders be matched? How reliably can drivers be activated? How efficiently can pricing balance demand and supply?

Robotaxis change the equation. Autonomy does not merely remove the human driver from the vehicle. It brings the vehicle, its capital structure, its charging needs, its maintenance cycle, its downtime risk, and its asset productivity much closer to the center of the business model.

2. The real disruption is economic, not technological

Most public discussion around robotaxis focuses on autonomous driving systems, sensors, AI models, safety performance, and regulatory approvals. These are critical. Without safe autonomy, there is no robotaxi market.

But the deeper disruption may be economic.

Traditional ride-hailing platforms optimized marketplace liquidity, driver availability, pricing efficiency, and customer acquisition. Robotaxi systems introduce an additional layer of operational complexity: vehicle financing, fleet ownership structures, charging infrastructure, depot operations, cleaning, maintenance, energy management, software-led dispatch, and depreciation management.

The app still matters. But in an autonomous mobility system, advantage increasingly depends on what happens beneath the app.

Who can finance fleets at the lowest cost? Who can keep vehicles earning for the highest share of the day? Who can reduce empty miles and charging downtime? Who can predict demand clusters and reposition vehicles before demand arrives? Who can extend asset life while preserving service reliability?

That is a very different playbook from the original ride-hailing model.

3. The economics are not solved yet

The most important point about robotaxis is also the most frequently missed: removing the driver does not automatically make the business profitable.

A recent paper in nature argues that existing robotaxi operations still appear to depend on investor subsidies, largely because the fully burdened cost base remains high. The cost stack includes not only the vehicle and autonomous driving hardware, but also R&D, sensor servicing and recalibration, remote monitoring, vehicle maintenance, insurance, and intensive data processing.

This matters because robotaxis shift the industry from a labor-marketplace problem to an asset-productivity problem. In the traditional ride-hailing model, much of the capital cost sits with drivers or fleet partners. In a robotaxi model, capital intensity, operational uptime, and asset utilization become central to the business case. For instance, analysts warn that Waymo – a leading Robotaxi player in the US – may take seven to eight years to break even on a fleet cash-flow basis. In once of the estimate, Waymo One fares in Los Angeles were lower than Uber and Lyft during surge periods, contributing to an estimated annual loss of about $34,000 per robotaxi under an optimistic support-staff assumption.

That does not mean robotaxis will fail. It means the economic threshold is higher than the technology narrative often suggests.

Robotaxi viability depends on a narrow set of operating variables: capacity utilization, annual mileage, labor ratio, wage rates, vehicle price, vehicle life, capital cost, maintenance intensity, and service-area design.

In other words, the question is not simply whether the vehicle can drive itself.

The real question is whether the fleet can earn enough miles, in the right places, with low enough downtime, at a cost structure that beats human-driven alternatives.

4. Fleet productivity becomes the new moat

In a human-driven ride-hailing marketplace, underutilization is partly absorbed by drivers. If a driver waits, refuels, maintains the car, or chooses not to work, the platform is affected through supply availability, but the vehicle-level economics are not always on the platform’s balance sheet.

In a robotaxi model, idle time is no longer just a marketplace inefficiency. It becomes an asset productivity problem.

A robotaxi is economically attractive only when it is used intensively, predictably, and efficiently. Every hour of idle time, every unnecessary repositioning mile, every avoidable charging delay, and every maintenance outage weakens the economics of the fleet.

That makes backend operations strategically central. Dispatch, charging, maintenance, cleaning, fleet balancing, and asset lifecycle management are no longer support functions. They become the economic engine of the business.

The future moat may therefore sit less in the visible user interface and more in the invisible operating system that keeps autonomous assets productive.

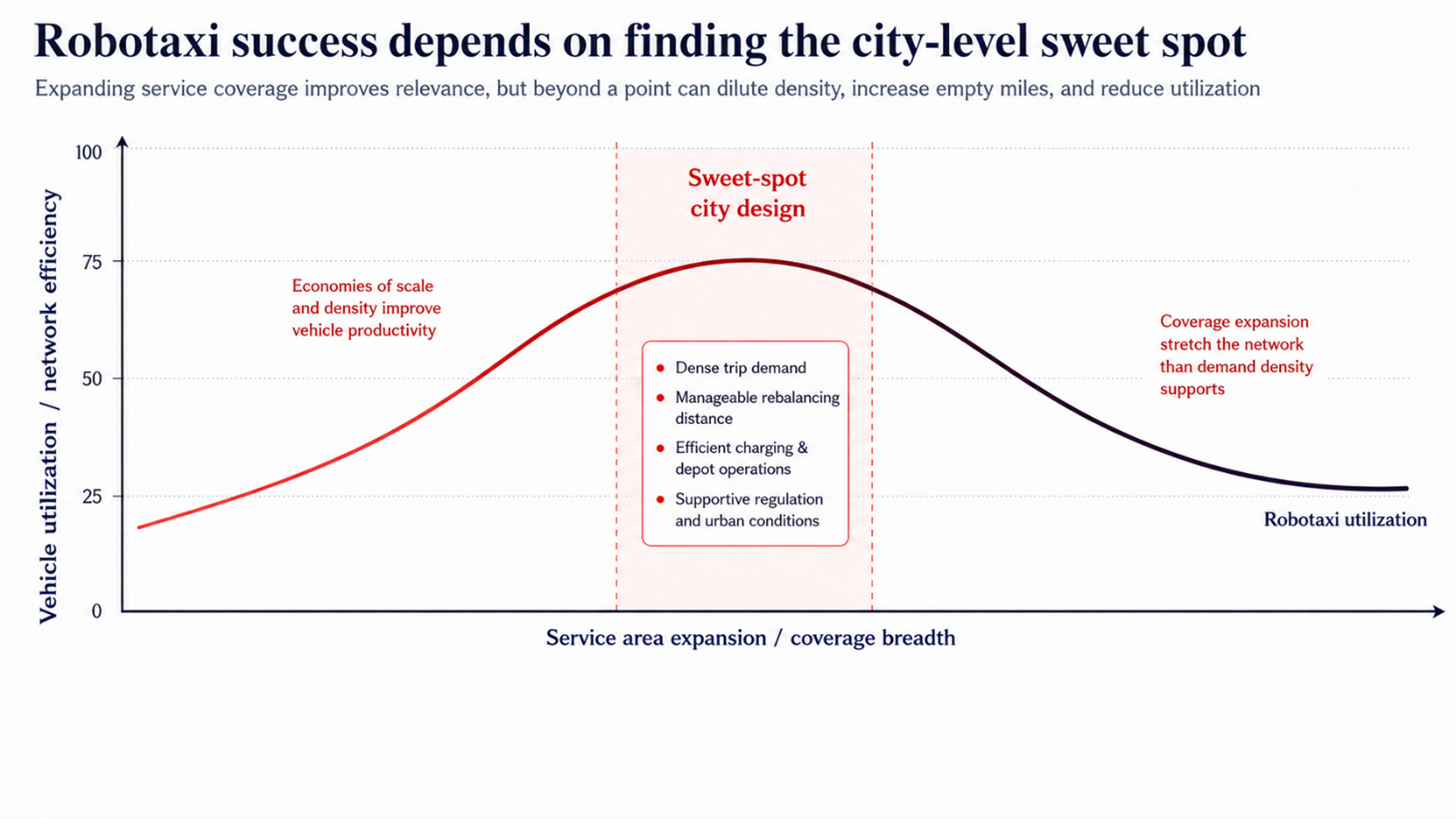

5. Density is not a detail. It is the business model.

Robotaxis benefit from both economies of scale and economies of urban density. Larger fleets can reduce capital and management costs per vehicle, while dense local demand can improve utilization and reduce empty mileage.

But this creates a difficult strategic trade-off. A robotaxi operator wants to expand service coverage because wider coverage improves consumer relevance. But wider coverage can also dilute density, increase repositioning miles, stretch charging and depot operations, and reduce utilization. Within a city, utilization depends not only on total demand but also on where trips start, where they end, how large the service area is, and how efficiently vehicles can be rebalanced.

This is why robotaxis may first work best in dense, tech-friendly urban environments with relatively strong demand concentration, manageable traffic conditions, and supportive regulation. In such cities, the operating model has a better chance of keeping vehicles productive for more hours of the day.

The implication is important: robotaxi rollout is not just a technology deployment plan. It is a city-level network design problem.

6. From ICE/CNG to EV to robotaxi: the operating transition

One way to understand this shift is to look at how fleet economics evolve across three mobility architectures.

In traditional ICE or CNG fleets, backend operations are important but largely administrative. The economics depend heavily on driver availability, fuel costs, financing arrangements, and demand utilization. Operational systems support the fleet, but they are rarely the primary source of differentiation.

EV fleets change this. Once fleets electrify, operations become more software-driven. Margins are shaped not only by fuel savings but by charging efficiency, vehicle scheduling, route-energy optimization, charger availability, and downtime reduction. The fleet operator’s ability to coordinate energy and utilization becomes materially more important.

Robotaxi fleets push the transition even further. In autonomous systems, backend operations effectively become the business model. The economics depend on real-time fleet intelligence, predictive maintenance, charging optimization, dynamic routing, asset lifecycle management, remote monitoring, and system-level utilization.

The operating transition can be summarized simply:

driver-led operations → energy optimization → system intelligence

That may become one of the defining mobility shifts of the next decade.

7. The cost curve is improving, but the operating-cost curve is uncertain

There are reasons to believe robotaxi economics can improve.

As fleets scale, vehicle capital costs and autonomous hardware costs may decline. Pony.ai’s seventh-generation robotaxi platform achieved a 70% reduction in bill-of-materials cost for its autonomous driving kit, with reductions driven by lower computing and LiDAR costs.[iii]

Real-world mileage can also improve the intelligence of autonomous systems. More miles create more exposure to edge cases such as extreme weather, bicycle lanes, construction zones, emergency vehicles, unusual pedestrian behavior, and complex intersections. Over time, this can improve driving performance and reduce operational friction.

But the decline in hardware cost does not automatically solve the business model.

The more uncertain side of the equation is operating cost: remote monitoring, maintenance, insurance, cleaning, charging operations, fleet balancing, customer support, data infrastructure, and regulatory compliance. The Nature Portfolio article explicitly notes that while capital costs may decline, the trajectory of operating costs remains less certain.

This is why the robotaxi race may not be won only by companies with superior autonomy software. It may be won by companies that can combine autonomy with low-cost operations, dense deployment, high utilization, and disciplined asset management.

8. Why recent industry moves matter

The robotaxi market is still early, but recent moves suggest major mobility players increasingly see autonomy as a strategic infrastructure layer rather than a side experiment.

Waymo’s expansion shows that robotaxi services can grow meaningfully when deployed in constrained, well-mapped, operationally supportive environments. The Nature Portfolio article notes that Waymo One’s business saw rapid growth, including expansion in Phoenix, San Francisco, and Los Angeles, with San Francisco market-share gains reported after August 2023.

At the same time, the withdrawal of several automakers from the robotaxi race is equally important. Ford and GM have stepped back from major robotaxi ambitions because of high costs and insufficient profitability, reinforcing that the sector is not merely a technology race but a capital discipline race.

The emerging structure may therefore be less about single-company vertical dominance and more about ecosystem specialization.

One player may provide the autonomous driving system. Another may own or finance the fleet. A platform may aggregate demand. A depot operator may handle charging, cleaning, and maintenance. A city may define the operating zone. An insurance partner may price liability. A data infrastructure provider may support fleet learning.

Robotaxis are becoming a systems business.

9. Why large-scale robotaxis remain difficult

The shift is strategically significant, but it is not easy.

Large-scale robotaxi deployment still faces regulatory uncertainty, safety validation requirements, edge-case driving complexity, infrastructure readiness, weather variability, urban mapping challenges, fleet financing intensity, and public trust barriers.

Even if autonomy technology improves rapidly, robotaxi economics still require extremely high utilization, dense routing, disciplined fleet management, reliable charging access, strong maintenance systems, and city-level operational consistency.

In many ways, the hardest challenge is not demonstrating that a vehicle can drive autonomously. It is proving that autonomous fleets can operate economically, repeatedly, and safely at city scale.

This is why robotaxis should be viewed less as a vehicle launch and more as a systems operation challenge.

10. India’s path may look different

North America and China currently lead large-scale robotaxi experimentation. India’s mobility evolution is likely to follow a different path.

Large-scale autonomous ride-hailing in India still appears structurally distant because of road variability, heterogeneous traffic behavior, infrastructure complexity, regulatory uncertainty, and dense mixed-use mobility environments.

But that does not mean India is outside the broader transition.

India is already evolving in adjacent directions: managed fleets, EV fleet operations, airport mobility, corporate transportation, premium bus systems, logistics fleet optimization, and software-led dispatch. These are not robotaxi markets yet, but they are training grounds for smarter fleet economics.

Before autonomy arrives at scale, Indian mobility operators may first learn to optimize utilization, manage EV charging economics, improve route productivity, reduce downtime, and operate fleets with greater software intelligence.

In that sense, India’s mobility transition may initially be less about robotaxis and more about progressively smarter fleet orchestration.

About TSR Lab

At TSR Lab, we work across the broader mobility landscape, from market assessments and operating model design to fleet economics, data strategy, utilization modeling, and growth decisions.

Our work spans multiple mobility architectures: ICE/CNG fleets, EV fleet systems, managed mobility networks, and emerging autonomous mobility models.

Because increasingly, the future of mobility may depend less on vehicles alone—and more on the intelligence and economics of the systems operating underneath them.

[i] Grand View Research. Robotaxi Market (2026-2033). https://www.grandviewresearch.com/industry-analysis/robotaxi-market-report

[ii] Wang, R., Zhong, C. & Guan, S. Recent developments of automated vehicles and local policy implications. npj. Sustain. Mobil. Transp. 3, 28 (2026). https://doi.org/10.1038/s44333-026-00095-3

[iii] PONY AI Inc. (2026). PONY AI Inc. Drives Commercialization at Scale with Lower-Cost Robotaxis and New L4 Light Truck. https://ir.pony.ai/news-releases/news-release-details/pony-ai-inc-drives-commercialization-scale-lower-cost-robotaxis